Trade #4 was a covered call expiring January 21, 2022. The covered call was on ATD.TO with a strike price of $49. I received a net premium of $139.05. This option expired worthless as the stock traded below $49 at expiration.

After that post, I did another trade.

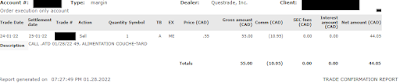

On January 24, I sold 1 Jan 28 2021 $49 Call at $0.55. I received net premium of $44.05 after commissions.

|

| Click to Enlarge |

On January 28th, the option was assigned as it traded in the money at expiration. When selling a call option, an option trading in the money means it trades above the strike price.

Summary:

In the original Savings Hack article, trade number 2 is the ATD.TO purchase of 100 shares.

Initial cost: = $4829.95

Option Assignment fee = $24.95

Net Option Premium = $44.05

Proceeds of Sale = $4900.00

Profit = Proceeds + premium - assignment fee - initial cost

= $4900.00 + $44.05 - $24.95 - $4829.95

= $89.15

This is capital gain I will report on taxes for the completion of this trade.

As per the above linked article, I transferred $300.18 to my savings. This $89.15 will be sent to my savings account. So that is a total of $389.33 to my savings.

DISCLAIMER

I am not a financial planner, financial advisor, accountant or tax attorney. The information on this blog represents my own thoughts and opinions and should NOT be taken as investment or business advice.

Every individual should do their due diligence to make their own financial decisions based on their financial situation and tolerance for risk.

I am not a financial planner, financial advisor, accountant or tax attorney. The information on this blog represents my own thoughts and opinions and should NOT be taken as investment or business advice.

Every individual should do their due diligence to make their own financial decisions based on their financial situation and tolerance for risk.